Questions and Answers About Nonbank Lenders Under Regulation U

5-840

Questions and Answers About Nonbank Lenders

Under Regulation U

The following questions and

answers on nonbank lenders under Regulation U are intended to provide

an introduction to the basic areas covered by the regulation. This

is not a complete discussion of all the requirements of the regulation

and is therefore not a substitute for the regulation itself.

1. Q. What is Regulation U?

A. Regulation U is a Federal Reserve Board regulation (12 CFR 221)

that sets out certain requirements for lenders other than brokers

and dealers extending credit secured by margin stock. (See question

9 for the definition of “margin stock.”)

5-841

2. Q. What

types of lenders are typically covered by Regulation U?

A. Regulation U covers not only commercial banks, but

also savings and loan associations, federal savings banks, credit

unions, production credit associations, insurance companies, and companies

with employee stock option plans.

5-842

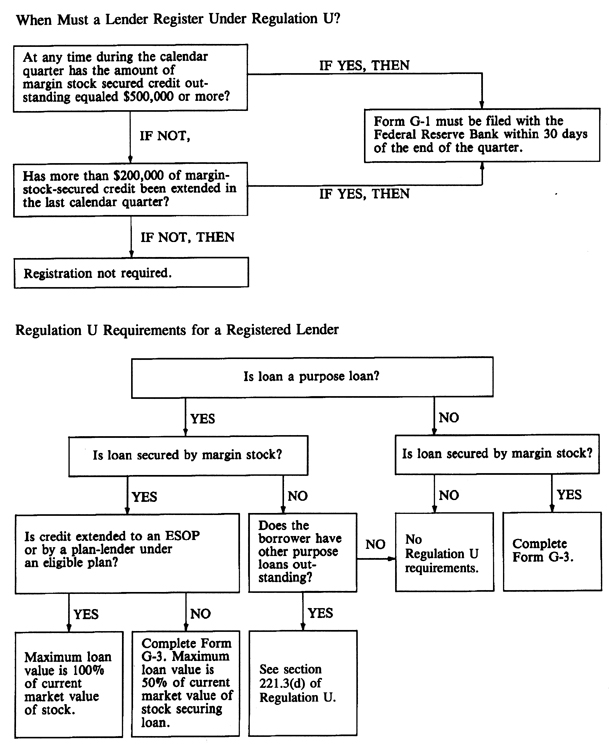

3. Q. When

does a lender become subject to Regulation U?

A. A commercial bank is always subject to Regulation U when it extends

credit secured by margin stock. A nonbank lender becomes subject to

Regulation U when it meets either one of the following threshold tests

for the amount of margin-stock-secured credit extended or outstanding.

Test 1: Has $200,000 or more in credit secured

directly or indirectly by margin stock been extended in the last calendar

quarter? If the answer is yes, the lender is subject to Regulation

U.

Test 2: At any time in the last quarter

has the amount of margin-stock-secured credit outstanding equalled

$500,000 or more? If yes, then the lender is subject to Regulation

U.

5-843

4. Q. If margin stock is taken as additional collateral

on a loan, is the loan considered in applying the two tests above?

A. Yes.

5-844

5. Q. What

happens when one of these tests is met?

A. The

lender must register with the Federal Reserve Bank in whose District

it is located by filling out and sending in Form G-1 (available by

calling the local Federal Reserve Bank) within 30 days of the end

of the calendar quarter in which one of the two tests is met. Sending

in the registration statement Form G-1 is a one-time requirement.

5-845

6. Q. Must such a lender register with the appropriate

Federal Reserve Bank even though it is regulated by the Office of

Thrift Supervision?

A. Yes, all nonbank, nonbroker

lenders must register with the Federal Reserve. Compliance with Regulation

U by savings and loans and federal savings banks has, since October

8, 1989, been monitored by the Office of Thrift Supervision.

5-846

7. Q. What is the Form G-1 and what information does it require

to be disclosed?

A. The Form G-1 is a simple

four-page form that must be filled out and submitted to the appropriate

Federal Reserve Bank by a lender in fulfillment of its requirement

to register as a nonbank lender whenever one of the tests mentioned

above is met (see question 3). The Form G-1 requires the registrant-lender

to provide the following information:

name of registrant

address of registrant

principal lines of business

form of business (corporation, partnership, etc.)

names of personnel responsible for maintaining company

records

purpose of credit extended

balance sheet

5-847

8. Q. What responsibilities does a lender take

on once it registers with a Federal Reserve Bank as a nonbank lender?

A. Regulation U has three important postregistration

requirements:

1. The nonbank lender must obtain from the borrower and

complete a purpose statement (Form G-3) for each loan secured by margin

stock.

2. The nonbank lender must adhere to margin requirements

(currently 50 percent) for purpose loans secured by margin stock (see

question 10 for the definition of “purpose loan”).

3. The nonbank lender must file an annual report of stock-secured

lending (Form G-4) as of each June 30.

5-848

9. Q. What is margin stock?

A. “Margin

stock” is defined in Regulation U (§ 221.2(i)) and includes (1) any

equity security registered on a national securities exchange, such

as the New York Stock Exchange or American Stock Exchange; (2) any

OTC security trading in the National Market System; (3) any warrant

or right to purchase a stock described in 1, 2, or 3 above; (4) any

debt security convertible into a stock described in 1, 2, or 3 above;

or (5) most mutual funds.

5-849

10. Q. What

is a purpose loan?

A. A purpose loan is a loan

whose proceeds are used to buy or carry margin stock. A loan to carry

margin stock is one that enables a borrower to maintain, reduce, or

retire indebtedness originally incurred to purchase margin stock.

5-850

11. Q. What are the Regulation U requirements for

purpose loans secured by margin stock?

A. The

first requirement is that the borrower complete the Form G-3 statement

of purpose, which must be signed by the borrower and a representative

of the lender. Second, a lender may not extend credit in excess of

the maximum loan value as specified in Regulation U. The maximum loan

value is now 50 percent of the current market value of the stock,

except for plan-lender loans, which are discussed in question 15.

In other words, the largest purpose loan a lender could extend would

be one-half the current market value of the margin stock securing

the loan (assuming the loan is secured only by margin stock). If a

purpose loan is initially in compliance with Regulation U, no action

is required by the lender if the market value of the stock changes

or if the maximum loan value as prescribed by Regulation U changes.

It should be noted that the stock securing the loan may be a different

stock from the stock that is purchased.

Other rules in Regulation U cover situations such as withdrawals

and substitutions of collateral, loan renewals, extensions of maturity,

and loan transfers. For these requirements, a lender should consult

the regulation or contact a Federal Reserve Bank.

5-851

12. Q. What is a nonpurpose loan under Regulation U?

A. A nonpurpose loan is a loan made for any purpose other than purchasing or carrying margin stock.

5-852

13. Q. What are the requirements of Regulation U for nonpurpose

loans?

A. The only Regulation U requirement

is that the borrower complete Form G-3 or Form U-1 if the loan is secured

(directly or indirectly) by margin stock. Regulation U places no restriction

on the amount of credit that may be extended on nonpurpose loans secured

by margin stock.

5-853

14. Q. What is Form G-3?

A. Form G-3 is a two-page form wherein the borrower

must disclose (1) the use to which the loan proceeds will be put,

(2) the amount of the loan, and (3) the collateral for the loan. The

form is signed by both the borrower and an authorized representative

of the lender and must be kept in the lender’s records for at least

three years after the termination of the credit.

5-854

15. Q. What is a plan-lender?

A. A plan-lender

is a corporation (including a wholly owned subsidiary, or a thrift

organization whose membership is limited to employees and former employees

of the corporation, its subsidiaries, or affiliates) that extends

credit to its employees, under an employee stock option plan approved

by the shareholders, to purchase stock of that corporation, its subsidiaries,

or affiliates. Loans under such a plan may be for any amount up to

100 percent of the current market value of the stock. A G-3 purpose

statement is not required for these loans.

5-855

16. Q. Does

Regulation U contain any special rules for employee stock ownership

plans (ESOPs)?

A. ESOPs qualified under section

401 of the Internal Revenue Code are entitled to exempt credit. A

nonbank lender may extend purpose credit to an ESOP without regard

to Regulation U, as long as the lender complies with the registration

requirements and files annual reports.

5-856

17. Q. Under

Regulation U, what reports must be filed with the Federal Reserve

Bank?

A. The registration form, Form G-1,

is discussed in question 7. An annual report, Form G-4, must be filed

within 30 days of June 30. This form will be supplied by the Reserve

Bank prior to June 30. The statement of purpose, Form G-3, should

be maintained in each borrower’s file. When a lender wants to deregister

and is eligible to do so, Form G-2, the deregistration statement,

must be filed with the Reserve Bank.

5-857

18. Q. When

is a lender eligible to deregister?

A. A registered

lender may deregister if, during the preceding six calendar months,

no more than $200,000 of credit secured by margin stock is outstanding.

5-858

19. Q. What is the effect of deregistering?

A. When a nonbank lender is eligible to deregister

and does so by filing a Form G-2, it ceases to become subject to the

requirements of Regulation U. Of course, if the lender extends margin-stock-secured

credit above the threshold amount, it would again have to register

with the Federal Reserve Bank.

5-859

20. Q. Where

can a lender get more information?

A. Copies

of Regulation U and Forms G-1, G-2, G-3, and G-4 may be obtained by

writing or calling the Federal Reserve Bank offices listed below: