(a) General. Under the SRWA, a Board-regulated institution’s

aggregate risk-weighted asset amount for its equity exposures is equal

to the sum of the risk-weighted asset amounts for each of the Board-regulated

institution’s individual equity exposures (other than equity

exposures to an investment fund) as determined in this section and

the risk-weighted asset amounts for each of the Board-regulated institution’s

individual equity exposures to an investment fund as determined in

section 217.154.

(b) SRWA computation for individual equity exposures. A Board-regulated

institution must determine the risk-weighted asset amount for an individual

equity exposure (other than an equity exposure to an investment fund)

by multiplying the adjusted carrying value of the equity exposure

or the effective portion and ineffective portion of a hedge pair (as

defined in paragraph (c) of this section) by the lowest applicable

risk weight in this section.

(1) Zero percent

risk weight equity exposures. An equity exposure to an entity

whose credit exposures are exempt from the 0.03 percent PD floor in

section 217.131(d)(2) is assigned a zero percent risk weight.

(2) 20 percent risk weight equity exposures. An equity exposure

to a Federal Home Loan Bank or the Federal Agricultural Mortgage Corporation

(Farmer Mac) is assigned a 20 percent risk weight.

(3) 100 percent

risk weight equity exposures. The following equity exposures

are assigned a 100 percent risk weight:

(i) Community development equity exposures.

(A) For state member banks and bank holding companies, an equity

exposure that qualifies as a community development investment under

12 U.S.C. 24 (Eleventh), excluding equity exposures to an unconsolidated

small business investment company and equity exposures held through

a consolidated small business investment company described in section

302 of the Small Business Investment Act of 1958 (15 U.S.C. 682).

(B) For savings and loan

holding companies, an equity exposure that is designed primarily to

promote community welfare, including the welfare of low- and moderate-income

communities or families, such as by providing services or employment,

and excluding equity exposures to an unconsolidated small business investment

company and equity exposures held through a small business investment

company described in section 302 of the Small Business Investment

Act of 1958 (15 U.S.C. 682).

(ii) Effective

portion of hedge pairs. The effective portion of a hedge pair.

(iii) Non-significant equity exposures. Equity

exposures, excluding significant investments in the capital of an

unconsolidated institution in the form of common stock and exposures

to an investment firm that would meet the definition of a traditional

securitization were it not for the Board’s application of paragraph

(8) of that definition in section 217.2 and has greater than immaterial

leverage, to the extent that the aggregate adjusted carrying value

of the exposures does not exceed 10 percent of the Board-regulated

institution’s total capital.

(A) To compute the aggregate

adjusted carrying value of a Board-regulated institution’s equity

exposures for purposes of this section, the Board-regulated institution

may exclude equity exposures described in paragraphs (b)(1), (b)(2),

(b)(3)(i), and (b)(3)(ii) of this section, the equity exposure in

a hedge pair with the smaller adjusted carrying value, and a proportion

of each equity exposure to an investment fund equal to the proportion

of the assets of the investment fund that are not equity exposures

or that meet the criterion of paragraph (b)(3)(i) of this section.

If a Board-regulated institution does not know the actual holdings

of the investment fund, the Board-regulated institution may calculate

the proportion of the assets of the fund that are not equity exposures

based on the terms of the prospectus, partnership agreement, or similar

contract that defines the fund’s permissible investments. If

the sum of the investment limits for all exposure classes within the

fund exceeds 100 percent, the Board-regulated institution must assume

for purposes of this section that the investment fund invests to the

maximum extent possible in equity exposures.

(B) When determining which of a Board-regulated

institution’s equity exposures qualifies for a 100 percent risk

weight under this section, a Board-regulated institution first must

include equity exposures to unconsolidated small business investment

companies or held through consolidated small business investment companies

described in section 302 of the Small Business Investment Act, then

must include publicly traded equity exposures (including those held

indirectly through investment funds), and then must include non-publicly

traded equity exposures (including those held indirectly through investment

funds).

(4) 250 percent

risk weight equity exposures. Significant investments in the

capital of unconsolidated financial institutions in the form of common

stock that are not deducted from capital pursuant to section 217.22(b)(4)are

assigned a 250 percent risk weight.

(5) 300 percent risk weight equity exposures. A publicly traded equity exposure (other than an equity exposure

described in paragraph (b)(7) of this section and including the ineffective

portion of a hedge pair) is assigned a 300 percent risk weight.

(6) 400

percent risk weight equity exposures. An equity exposure (other

than an equity exposure described in paragraph (b)(7) of this section)

that is not publicly traded is assigned a 400 percent risk weight.

(7) 600 percent risk weight equity exposures. An equity exposure to an investment firm that:

(i) Would

meet the definition of a traditional securitization were it not for

the Board’s application of paragraph (8) of that definition

in section 217.2; and

(ii) Has greater than immaterial leverage is assigned a 600 percent

risk weight.

(c) Hedge transactions.

(1) Hedge pair. A hedge pair is two equity exposures that form an effective hedge

so long as each equity exposure is publicly traded or has a return

that is primarily based on a publicly traded equity exposure.

(2) Effective hedge. Two equity exposures form an effective hedge

if the exposures either have the same remaining maturity or each has

a remaining maturity of at least three months; the hedge relationship

is formally documented in a prospective manner (that is, before the

Board-regulated institution acquires at least one of the equity exposures);

the documentation specifies the measure of effectiveness (E) the Board-regulated

institution will use for the hedge relationship throughout the life

of the transaction; and the hedge relationship has an E greater than

or equal to 0.8. A Board-regulated institution must measure E at least

quarterly and must use one of three alternative measures of E:

(i) Under the dollar-offset method of measuring effectiveness, the

Board-regulated institution must determine the ratio of value change

(RVC). The RVC is the ratio of the cumulative sum of the periodic

changes in value of one equity exposure to the cumulative sum of the

periodic changes in the value of the other equity exposure. If RVC

is positive, the hedge is not effective and E equals zero. If RVC

is negative and greater than or equal to −1 (that is, between

zero and −1), then E equals the absolute value of RVC. If RVC

is negative and less than −1, then E equals 2 plus RVC.

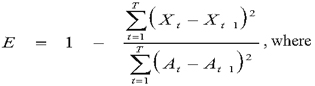

(ii) Under the variability-reduction

method of measuring effectiveness:

Figure 1. DISPLAY EQUATION

$$

E = 1 - \frac{{\sum\limits^T_{t=1}} \bigg( X_t - X_{t-1} \bigg)^2}

{{\sum\limits^T_{t=1}} \bigg( A_t - A_{t-1} \bigg)^2 }

\text{ , where}

$$

(A) X t = A t − B t;

(B) A t = the value at time t of one exposure in a hedge pair; and

(C) B t = the value at time t of the other exposure in a hedge pair.

(iii)

Under the regression method of measuring effectiveness, E equals the

coefficient of determination of a regression in which the change in

value of one exposure in a hedge pair is the dependent variable and

the change in value of the other exposure in a hedge pair is the independent

variable. However, if the estimated regression coefficient is positive,

then the value of E is zero.

(3) The effective portion of a hedge pair

is E multiplied by the greater of the adjusted carrying values of

the equity exposures forming a hedge pair.

(4) The ineffective portion of a hedge

pair is (1−E) multiplied by the greater of the adjusted carrying

values of the equity exposures forming a hedge pair.