SECTION 217.131—Mechanics

for Calculating Total Wholesale and Retail Risk-Weighted Assets

(a) Overview. A Board-regulated

institution must calculate its total wholesale and retail risk-weighted

asset amount in four distinct phases:

(1) Phase 1—categorization of exposures;

(2) Phase 2—assignment

of wholesale obligors and exposures to rating grades and segmentation

of retail exposures;

(3) Phase 3—assignment of risk parameters to wholesale exposures

and segments of retail exposures; and

(4) Phase 4—calculation of risk-weighted

asset amounts.

(b) Phase 1—Categorization. The Board-regulated

institution must determine which of its exposures are wholesale exposures,

retail exposures, securitization exposures, or equity exposures.

The Board-regulated institution must categorize each retail exposure

as a residential mortgage exposure, a QRE, or another retail exposure.

The Board-regulated institution must identify which wholesale exposures

are HVCRE exposures, sovereign exposures, OTC derivative contracts,

repo-style transactions, eligible margin loans, eligible purchased

wholesale exposures, cleared transactions, default fund contributions,

and unsettled transactions to which section 217.136 applies, and eligible

guarantees or eligible credit derivatives that are used as credit

risk mitigants. The Board-regulated institution must identify any

on-balance sheet asset that does not meet the definition of a wholesale,

retail, equity, or securitization exposure, any non-material portfolio

of exposures described in paragraph (e)(4) of this section, and for

bank holding companies and savings and loan holding companies, any

on-balance sheet asset that is held in a non-guaranteed separate account.

(c) Phase 2—Assignment

of wholesale obligors and exposures to rating grades and retail exposures

to segments.

(1) Assignment

of wholesale obligors and exposures to rating grades.

(i) The

Board-regulated institution must assign each obligor of a wholesale

exposure to a single obligor rating grade and must assign each wholesale

exposure to which it does not directly assign an LGD estimate to a

loss severity rating grade.

(ii) The Board-regulated institution

must identify which of its wholesale obligors are in default.

(2) Segmentation of retail exposures.

(i) The Board-regulated

institution must group the retail exposures in each retail subcategory

into segments that have homogeneous risk characteristics.

(ii) The Board-regulated

institution must identify which of its retail exposures are in default.

The Board-regulated institution must segment defaulted retail exposures

separately from non-defaulted retail exposures.

(iii) If the Board-regulated institution

determines the EAD for eligible margin loans using the approach in

section 217.132(b), the Board-regulated institution must identify

which of its retail exposures are eligible margin loans for which

the Board-regulated institution uses this EAD approach and must segment

such eligible margin loans separately from other retail exposures.

(3) Eligible purchased wholesale exposures. A Board-regulated institution may group its eligible purchased wholesale

exposures into segments that have homogeneous risk characteristics.

A Board-regulated institution must use the wholesale exposure formula

in Table 1 of this section to determine the risk-based capital requirement

for each segment of eligible purchased wholesale exposures.

(d) Phase 3—Assignment of

risk parameters to wholesale exposures and segments of retail exposures.

(1) Quantification process. Subject to the limitations in this paragraph

(d), the Board-regulated institution must:

(i) Associate a PD

with each wholesale obligor rating grade;

(ii) Associate an LGD with each wholesale

loss severity rating grade or assign an LGD to each wholesale exposure;

(iii) Assign an EAD

and M to each wholesale exposure; and

(iv) Assign a PD, LGD, and EAD to each

segment of retail exposures.

(2) Floor on

PD assignment. The PD for each wholesale obligor or retail segment

may not be less than 0.03 percent, except for exposures to or directly

and unconditionally guaranteed by a sovereign entity, the Bank for

International Settlements, the International Monetary Fund, the European

Commission, the European Central Bank, the European Stability Mechanism,

the European Financial Stability Facility, or a multilateral development

bank, to which the Board-regulated institution assigns a rating grade

associated with a PD of less than 0.03 percent.

(3) Floor on

LGD estimation. The LGD for each segment of residential mortgage

exposures may not be less than 10 percent, except for segments of

residential mortgage exposures for which all or substantially all

of the principal of each exposure is either:

(i) Directly and unconditionally

guaranteed by the full faith and credit of a sovereign entity; or

(ii) Guaranteed by

a contingent obligation of the U.S. government or its agencies, the

enforceability of which is dependent upon some affirmative action

on the part of the beneficiary of the guarantee or a third party (for

example, meeting servicing requirements).

(4) Eligible purchased wholesale exposures. A Board-regulated institution

must assign a PD, LGD, EAD, and M to each segment of eligible purchased

wholesale exposures. If the Board-regulated institution can estimate

ECL (but not PD or LGD) for a segment of eligible purchased wholesale

exposures, the Board-regulated institution must assume that the LGD

of the segment equals 100 percent and that the PD of the segment equals

ECL divided by EAD. The estimated ECL must be calculated for the exposures

without regard to any assumption of recourse or guarantees from the

seller or other parties.

(5) Credit risk mitigation: credit derivatives,

guarantees, and collateral.

(i) A Board-regulated institution

may take into account the risk reducing effects of eligible guarantees

and eligible credit derivatives in support of a wholesale exposure

by applying the PD substitution or LGD adjustment treatment to the

exposure as provided in section 217.134 or, if applicable, applying

double default treatment to the exposure as provided in section 217.135.

A Board-regulated institution may decide separately for each wholesale

exposure that qualifies for the double default treatment under section

217.135 whether to apply the double default treatment or to use the

PD substitution or LGD adjustment treatment without recognizing double

default effects.

(ii) A Board-regulated institution may take into account the risk

reducing effects of guarantees and credit derivatives in support of

retail exposures in a segment when quantifying the PD and LGD of the

segment. In doing so, a Board-regulated institution must consider

all relevant available information.

(iii) Except as provided in paragraph

(d)(6) of this section, a Board-regulated institution may take into

account the risk reducing effects of collateral in support of a wholesale

exposure when quantifying the LGD of the exposure, and may take into

account the risk reducing effects of collateral in support of retail

exposures when quantifying the PD and LGD of the segment. In order

to do so, a Board-regulated institution must have established internal

requirements for collateral management, legal certainty, and risk

management processes.

(6) EAD for OTC

derivative contracts, repo-style transactions, and eligible margin

loans. A Board-regulated institution must calculate its EAD for

an OTC derivative contract as provided in section 217.132 (c) and

(d). A Board-regulated institution may take into account the risk-reducing

effects of financial collateral in support of a repo-style transaction

or eligible margin loan and of any collateral in support of a repo-style

transaction that is included in the Board-regulated institution’s

VaR-based measure under subpart F of this part through an adjustment

to EAD as provided in section 217.132(b) and (d). A Board-regulated

institution that takes collateral into account through such an adjustment

to EAD under section 217.132 may not reflect such collateral in LGD.

(7) Effective maturity. An exposure’s M must

be no greater than five years and no less than one year, except that

an exposure’s M must be no less than one day if the exposure is a

trade related letter of credit, or if the exposure has an original

maturity of less than one year and is not part of a Board-regulated

institution’s ongoing financing of the obligor. An exposure is not

part of a Board-regulated institution’s ongoing financing of the obligor

if the Board-regulated institution:

(i) Has a legal and practical

ability not to renew or roll over the exposure in the event of credit

deterioration of the obligor;

(ii) Makes an independent credit decision at the

inception of the exposure and at every renewal or roll over; and

(iii) Has no substantial

commercial incentive to continue its credit relationship with the

obligor in the event of credit deterioration of the obligor.

(8) EAD for exposures to certain central counterparties. A Board-regulated institution may attribute an EAD of zero to exposures

that arise from the settlement of cash transactions (such as equities,

fixed income, spot foreign exchange, and spot commodities) with a

central counterparty where there is no assumption of ongoing counterparty

credit risk by the central counterparty after settlement of the trade

and associated default fund contributions.

(e) Phase 4—Calculation of risk-weighted

assets.

(1) Non-defaulted

exposures.

(i) A Board-regulated institution must

calculate the dollar risk-based capital requirement for each of its

wholesale exposures to a non-defaulted obligor (except for eligible

guarantees and eligible credit derivatives that hedge another wholesale

exposure, IMM exposures, cleared transactions, default fund contributions,

unsettled transactions, and exposures to which the Board-regulated

institution applies the double default treatment in section 217.135)

and segments of non-defaulted retail exposures by inserting the assigned

risk parameters for the wholesale obligor and exposure or retail segment

into the appropriate risk-based capital formula specified in Table

1 and multiplying the output of the formula (K) by the EAD of the

exposure or segment. Alternatively, a Board-regulated institution

may apply a 300 percent risk weight to the EAD of an eligible margin

loan if the Board-regulated institution is not able to meet the Board’s

requirements for estimation of PD and LGD for the margin loan.

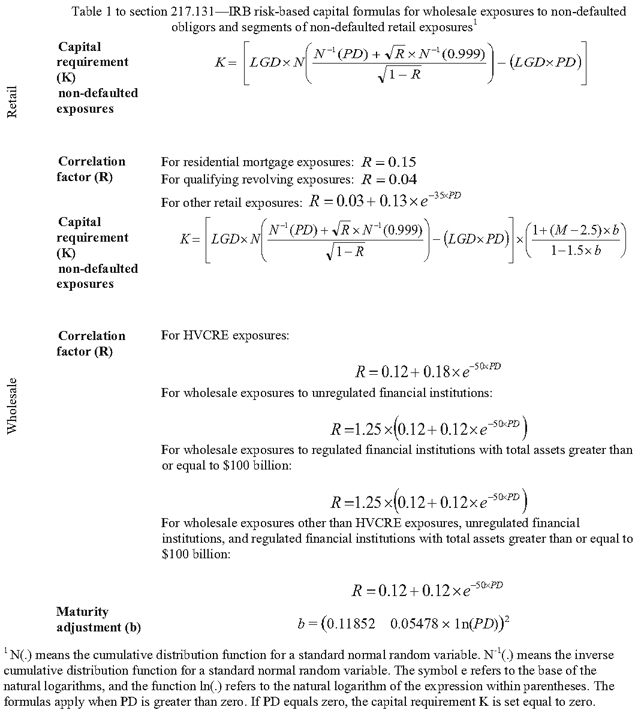

Figure 1. DISPLAY EQUATION

$$

\begin{align*}

\tiny

&\qquad\textbf{Retail} \\

&\textbf{Capital} & &\qquad\qquad K = \Bigg[ \small{LGD} \times N \Bigg\lgroup \frac{N^{-1}(PD) + \sqrt{R} \times N^{-1} (0.999)}{\sqrt{1-R}} \Bigg\rgroup - (\small{LGD} \times \small{PD}) \Bigg]\\

& \textbf{requirement} \\

& \textbf{(K)} \\

& \textbf{non-defaulted} \\

& \textbf{exposures} \\

\\

\\

&\textbf{Correlation} & &\text{For residential mortgage exposures: R= 0.15}\\

&\textbf{factor (R)} & &\text{For qualifying revolving exposures: R= 0.04}\\

& & &\text{For other retail exposures: }R= 0.03 + 0.13\times e^{-35xPD}\\

&\textbf{Capital} & & \small{K} = \Bigg[ \small{LGD} \times N \Bigg\lgroup \frac{N^{-1}(PD) + \sqrt{R} \times N^{-1} (0.999)}{\sqrt{1-R}} \Bigg\rgroup - (\small{LGD} \times \small{PD}) \Bigg] \times \Bigg\lgroup \frac{1+ (M - 2.5) \times b}{1-1.5 \times b} \Bigg\rgroup\\

& \textbf{requirement} \\

& \textbf{(K)} \\

& \textbf{non-defaulted} \\

& \textbf{exposures} \\

\\

\\

\\&\qquad\textbf{Wholesale} \\

\\&\textbf{Correlation} & &\text{For HVCRE exposures:}\\

\\&\textbf{factor (R)} & & \qquad\qquad\qquad\qquad R = 0.12 + 0.18 \times e^{-50 \times PD}\\

\\& & &\text{For wholesale exposures to unregulated financial institutions:}\\

\\& & & \qquad\qquad\qquad\qquad R = 1.25 \times \bigg( 0.12 + 0.12 \times e^{-50 \times PD} \bigg)\\

\\& & &\text{For wholesale exposures to regulated financial institutions with total}\\

\\& & &\text{assets greater than or equal to \$100 billion:}\\

\\& & &\qquad\qquad\qquad\qquad R = 1.25 \times \bigg( 0.12 + 0.12 \times e^{-50 \times PD} \bigg)\\

\\& & &\text{For wholesale exposures other than HVCRE exposures, unregulated financial}\\

\\& & &\text{institutions, and regulated financial institutions with total assets greater}\\

\\& & &\text{than or equal to \$100 billion:}\\

\\& & & \qquad\qquad\qquad\qquad R = 0.12 + 0.12 \times e^{-50 \times PD}\\

\\

&\textbf{Maturity} & & \qquad\qquad\qquad b = \big(0.11852 - 0.05478 \times 1\mathrm{n}(PD)\big)^2\\

&\textbf{adjustment (b)}

\\

\end{align*}

$$

(ii) The sum of all the dollar risk-based capital requirements for

each wholesale exposure to a non-defaulted obligor and segment of

non-defaulted retail exposures calculated in paragraph (e)(1)(i) of

this section and in section 217.135(e) equals the total dollar risk-based

capital requirement for those exposures and segments.

(iii) The aggregate risk-weighted

asset amount for wholesale exposures to non-defaulted obligors and

segments of non-defaulted retail exposures equals the total dollar

risk-based capital requirement in paragraph (e)(1)(ii) of this section

multiplied by 12.5.

(2) Wholesale exposures to defaulted obligors

and segments of defaulted retail exposures.

(i) Not covered by an eligible U.S. government guarantee: The dollar risk-based capital requirement for each wholesale exposure

not covered by an eligible guarantee from the U.S. government to a

defaulted obligor and each segment of defaulted retail exposures not

covered by an eligible guarantee from the U.S. government equals 0.08

multiplied by the EAD of the exposure or segment.

(ii) Covered by an eligible U.S. government guarantee: The dollar risk-based capital requirement for each wholesale exposure

to a defaulted obligor covered by an eligible guarantee from the U.S.

government and each segment of defaulted retail exposures covered

by an eligible guarantee from the U.S. government equals the sum of:

(A) The sum of the EAD of the portion of each wholesale exposure

to a defaulted obligor covered by an eligible guarantee from the U.S.

government plus the EAD of the portion of each segment of defaulted

retail exposures that is covered by an eligible guarantee from the

U.S. government and the resulting sum is multiplied by 0.016, and

(B) The sum of the EAD of

the portion of each wholesale exposure to a defaulted obligor not

covered by an eligible guarantee from the U.S. government plus the

EAD of the portion of each segment of defaulted retail exposures that

is not covered by an eligible guarantee from the U.S. government and

the resulting sum is multiplied by 0.08.

(iii) The sum of all the

dollar risk-based capital requirements for each wholesale exposure

to a defaulted obligor and each segment of defaulted retail exposures

calculated in paragraph (e)(2)(i) of this section plus the dollar

risk-based capital requirements each wholesale exposure to a defaulted

obligor and for each segment of defaulted retail exposures calculated

in paragraph (e)(2)(ii) of this section equals the total dollar risk-based

capital requirement for those exposures and segments.

(iv) The aggregate risk-weighted asset

amount for wholesale exposures to defaulted obligors and segments

of defaulted retail exposures equals the total dollar risk-based capital

requirement calculated in paragraph (e)(2)(iii) of this section multiplied

by 12.5.

(3) Assets not included in a defined exposure

category.

(i) A bank holding company or savings

and loan holding company may assign a risk-weighted asset amount of

zero to cash owned and held in all offices of subsidiary depository

institutions or in transit; and for gold bullion held in a subsidiary

depository institution’s own vaults, or held in another depository

institution’s vaults on an allocated basis, to the extent the gold

bullion assets are offset by gold bullion liabilities.

(ii) A state member bank

may assign a risk-weighted asset amount to cash owned and held in

all offices of the state member bank or in transit and for gold bullion

held in the state member bank’s own vaults, or held in another depository

institution’s vaults on an allocated basis, to the extent the gold

bullion assets are offset by gold bullion liabilities.

(iii) A Board-regulated

institution must assign a risk-weighted asset amount equal to 50 percent

of the carrying value to a pre-sold construction loan unless the purchase

contract is cancelled, in which case a Board-regulated institution

must assign a risk-weighted asset amount equal to a 100 percent of

the carrying value of the pre-sold construction loan.

(iv) The risk-weighted asset amount

for the residual value of a retail lease exposure equals such residual

value.

(v) The risk-weighted

asset amount for DTAs arising from temporary differences that the

Board-regulated institution could realize through net operating loss

carrybacks equals the carrying value, netted in accordance with section

217.22.

(vi) The

risk-weighted asset amount for MSAs, DTAs arising from temporary timing

differences that the Board-regulated institution could not realize

through net operating loss carrybacks, and significant investments

in the capital of unconsolidated financial institutions in the form

of common stock that are not deducted pursuant to section 217.22(a)(7)

equals the amount not subject to deduction multiplied by 250 percent.

(vii) The risk-weighted

asset amount for any other on-balance-sheet asset that does not meet

the definition of a wholesale, retail, securitization, IMM, or equity exposure,

cleared transaction, or default fund contribution and is not subject

to deduction under section 217.22(a), (c), or (d) equals the carrying

value of the asset.

(viii) The

risk-weighted asset amount for a Paycheck Protection Program covered

loan as defined in section 7(a)(36) of the Small Business Act (15

U.S.C. 636(a)(36)) equals zero.

(4) Non-material portfolios of exposures. The risk-weighted asset

amount of a portfolio of exposures for which the Board-regulated institution

has demonstrated to the Board’s satisfaction that the portfolio (when

combined with all other portfolios of exposures that the Board-regulated

institution seeks to treat under this paragraph (e)) is not material

to the Board-regulated institution is the sum of the carrying values

of on-balance sheet exposures plus the notional amounts of off-balance

sheet exposures in the portfolio. For purposes of this paragraph (e)(4),

the notional amount of an OTC derivative contract that is not a credit

derivative is the EAD of the derivative as calculated in section 217.132.

(5) Assets held in non-guaranteed separate accounts. The risk-weighted asset amount for an on-balance sheet asset that

is held in a non-guaranteed separate account is zero percent of the

carrying value of the asset.