(a) Scope.

(1) General. A Board-regulated institution may recognize the credit risk mitigation

benefits of an eligible guarantee or eligible credit derivative by

substituting the risk weight associated with the protection provider

for the risk weight assigned to an exposure, as provided under this

section.

(2) This section

applies to exposures for which:

(i) Credit risk is fully

covered by an eligible guarantee or eligible credit derivative; or

(ii) Credit risk is

covered on a pro rata basis (that is, on a basis in which the Board-regulated

institution and the protection provider share losses proportionately)

by an eligible guarantee or eligible credit derivative.

(3) Exposures on which

there is a tranching of credit risk (reflecting at least two different

levels of seniority) generally are securitization exposures subject

to sections 217.41 through 217.45.

(4) If multiple eligible guarantees or

eligible credit derivatives cover a single exposure described in this

section, a Board-regulated institution may treat the hedged exposure

as multiple separate exposures each covered by a single eligible guarantee

or eligible credit derivative and may calculate a separate risk-weighted

asset amount for each separate exposure as described in paragraph

(c) of this section.

(5) If a single eligible guarantee or eligible credit derivative

covers multiple hedged exposures described in paragraph (a)(2) of

this section, a Board-regulated institution must treat each hedged

exposure as covered by a separate eligible guarantee or eligible credit

derivative and must calculate a separate risk-weighted asset amount

for each exposure as described in paragraph (c) of this section.

(b) Rules of

recognition.

(1) A Board-regulated institution may only

recognize the credit risk mitigation benefits of eligible guarantees

and eligible credit derivatives.

(2) A Board-regulated institution may only

recognize the credit risk mitigation benefits of an eligible credit

derivative to hedge an exposure that is different from the credit

derivative’s reference exposure used for determining the derivative’s

cash settlement value, deliverable obligation, or occurrence of a

credit event if:

(i) The reference exposure ranks pari passu with, or is subordinated to, the hedged exposure;

and

(ii) The reference

exposure and the hedged exposure are to the same legal entity, and

legally enforceable cross-default or cross-acceleration clauses are

in place to ensure payments under the credit derivative are triggered

when the obligated party of the hedged exposure fails to pay under

the terms of the hedged exposure.

(c) Substitution approach.

(1) Full coverage. If an eligible guarantee or eligible credit derivative meets the

conditions in paragraphs (a) and (b) of this section and the protection

amount (P) of the guarantee or credit derivative is greater than or

equal to the exposure amount of the hedged exposure, a Board-regulated

institution may recognize the guarantee or credit derivative in determining

the risk-weighted asset amount for the hedged exposure by substituting

the risk weight applicable to the guarantor or credit derivative protection

provider under this subpart D for the risk weight assigned to the

exposure.

(2) Partial coverage. If an eligible guarantee

or eligible credit derivative meets the conditions in paragraphs (a)

and (b) of this section and the protection amount (P) of the guarantee

or credit derivative is less than the exposure amount of the hedged

exposure, the Board-regulated institution must treat the hedged exposure

as two separate exposures (protected and unprotected) in order to

recognize the credit risk mitigation benefit of the guarantee or credit

derivative.

(i) The

Board-regulated institution may calculate the risk-weighted asset

amount for the protected exposure under this subpart D, where the

applicable risk weight is the risk weight applicable to the guarantor

or credit derivative protection provider.

(ii) The Board-regulated institution

must calculate the risk-weighted asset amount for the unprotected

exposure under this subpart D, where the applicable risk weight is

that of the unprotected portion of the hedged exposure.

(iii) The treatment provided in this

section is applicable when the credit risk of an exposure is covered

on a partial pro rata basis and may be applicable when an adjustment

is made to the effective notional amount of the guarantee or credit

derivative under paragraphs (d), (e), or (f) of this section.

(d) Maturity

mismatch adjustment.

(1) A Board-regulated institution that

recognizes an eligible guarantee or eligible credit derivative in

determining the risk-weighted asset amount for a hedged exposure must

adjust the effective notional amount of the credit risk mitigant to

reflect any maturity mismatch between the hedged exposure and the

credit risk mitigant.

(2) A maturity mismatch occurs when the residual maturity of a credit

risk mitigant is less than that of the hedged exposure(s).

(3) The residual maturity of

a hedged exposure is the longest possible remaining time before the

obligated party of the hedged exposure is scheduled to fulfil its

obligation on the hedged exposure. If a credit risk mitigant has embedded

options that may reduce its term, the Board-regulated institution

(protection purchaser) must use the shortest possible residual maturity

for the credit risk mitigant. If a call is at the discretion of the

protection provider, the residual maturity of the credit risk mitigant

is at the first call date. If the call is at the discretion of the

Board-regulated institution (protection purchaser), but the terms

of the arrangement at origination of the credit risk mitigant contain

a positive incentive for the Board-regulated institution to call the

transaction before contractual maturity, the remaining time to the

first call date is the residual maturity of the credit risk mitigant.

(4) A credit risk mitigant

with a maturity mismatch may be recognized only if its original maturity

is greater than or equal to one year and its residual maturity is

greater than three months.

(5) When a maturity mismatch exists, the

Board-regulated institution must apply the following adjustment to

reduce the effective notional amount of the credit risk mitigant:

Pm = E × (t−0.25)/(T−0.25), where:

(i) Pm = effective notional

amount of the credit risk mitigant, adjusted for maturity mismatch;

(ii) E = effective

notional amount of the credit risk mitigant;

(iii) t = the lesser of T or the residual

maturity of the credit risk mitigant, expressed in years; and

(iv) T = the lesser of

five or the residual maturity of the hedged exposure, expressed in

years.

(e) Adjustment for credit derivatives without restructuring

as a credit event. If a Board-regulated institution recognizes

an eligible credit derivative that does not include as a credit event

a restructuring of the hedged exposure involving forgiveness or postponement

of principal, interest, or fees that results in a credit loss event

(that is, a charge-off, specific provision, or other similar debit

to the profit and loss account), the Board-regulated institution must

apply the following adjustment to reduce the effective notional amount

of the credit derivative: Pr = Pm × 0.60, where:

(1) Pr = effective notional amount of the

credit risk mitigant, adjusted for lack of restructuring event (and

maturity mismatch, if applicable); and

(2) Pm = effective notional amount of the

credit risk mitigant (adjusted for maturity mismatch, if applicable).

(f) Currency

mismatch adjustment.

(1) If a Board-regulated institution recognizes

an eligible guarantee or eligible credit derivative that is denominated

in a currency different from that in which the hedged exposure is

denominated, the Board-regulated institution must apply the following

formula to the effective notional amount of the guarantee or credit

derivative: Pc = Pr × (1-HFX), where:

(i) Pc =

effective notional amount of the credit risk mitigant, adjusted for

currency mismatch (and maturity mismatch and lack of restructuring

event, if applicable);

(ii) Pr = effective notional amount of the credit risk mitigant (adjusted

for maturity mismatch and lack of restructuring event, if applicable);

and

(iii) HFX = haircut appropriate for the currency mismatch between

the credit risk mitigant and the hedged exposure.

(2) A Board-regulated

institution must set HFX equal to eight percent unless

it qualifies for the use of and uses its own internal estimates of

foreign exchange volatility based on a ten-business-day holding period.

A Board-regulated institution qualifies for the use of its own internal

estimates of foreign exchange volatility if it qualifies for the use

of its own-estimates haircuts in section 217.37(c)(4).

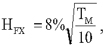

(3) A Board-regulated institution

must adjust HFX calculated in paragraph (f)(2) of this

section upward if the Board-regulated institution revalues the guarantee

or credit derivative less frequently than once every 10 business days

using the following square root of time formula:

Figure 1. DISPLAY EQUATION

$$

\mathrm{H_{FX} = 8\% \sqrt{\frac{T_M}{10}}} \text{ ,}

$$

where TM equals the greater of 10 or the number of days between revaluation.