The Board of Governors of the Federal Reserve System

(Board), the Federal Deposit Insurance Corporation (FDIC), and the

Office of the Comptroller of the Currency (OCC) (collectively, “the

agencies”) have issued this guidance to provide sound risk-management

principles supervised banking organizations1 can leverage when developing and implementing

risk-management practices to assess and manage risks associated with

third-party relationships.2

Whether activities are performed internally or via a third

party, banking organizations are required to operate in a safe and

sound manner3 and in compliance

with applicable laws and regulations.4 A banking organization’s use of third parties does

not diminish its responsibility to meet these requirements to the

same extent as if its activities were performed by the banking organization

in-house. To operate in a safe and sound manner, a banking organization

establishes risk management practices to effectively manage the risks

arising from its activities, including from third-party relationships.5

This guidance addresses any business

arrangement6 between a banking organization and another entity, by contract

or otherwise. A third-party relationship may exist despite a lack

of a contract or remuneration. Third-party relationships can include,

but are not limited to, outsourced services, use of independent consultants,

referral arrangements, merchant payment processing services, services

provided by affiliates and subsidiaries, and joint ventures. Some

banking organizations may form third-party relationships with new

or novel structures and features—such as those observed in relationships

with some financial technology (fintech) companies. The respective

roles and responsibilities of a banking organization and a third party

may differ, based on the specific circumstances of the relationship.

Where the third-party relationship involves the provision of products

or services to, or other interaction with, customers, the banking

organization and the third party may have varying degrees of interaction

with those customers.

The use of third parties can offer banking organizations

significant benefits, such as access to new technologies, human capital,

delivery channels, products, services, and markets. However, the use

of third parties can reduce a banking organization’s direct control

over activities and may introduce new risks or increase existing risks,

such as operational, compliance, and strategic risks. Increased risk

often arises from greater operational or technological complexity,

newer or different types of relationships, or potential inferior performance

by the third party. A banking organization can be exposed to adverse

impacts, including substantial financial loss and operational disruption,

if it fails to appropriately manage the risks associated with third-party

relationships. Therefore, it is important for a banking organization

to identify, assess, monitor, and control risks related to third-party

relationships.

The principles set forth in this guidance can support

effective third-party risk management for all types of third-party

relationships, regardless of how they may be structured. It is important

for a banking organization to understand how the arrangement with

a particular third party is structured so that the banking organization

may assess the types and levels of risks posed and determine how to

manage the third-party relationship accordingly.

B. Risk Management

Not all relationships present the same level of risk,

and therefore not all relationships require the same level or type

of oversight or risk management. As part of sound risk management,

a banking organization analyzes the risks associated with each third-party

relationship and tailors risk-management practices, commensurate with

the banking organization’s size, complexity, and risk profile and

with the nature of the third-party relationship. Maintaining a complete

inventory of its third-party relationships and periodically conducting

risk assessments for each third-party relationship supports a banking

organization’s determination of whether risks have changed over time

and to update risk-management practices accordingly.

As part of sound risk management, banking organizations

engage in more comprehensive and rigorous oversight and management

of third-party relationships that support higher-risk activities,

including critical activities. Characteristics of critical activities

may include those activities that could:

cause a banking organization to face

significant risk if the third party fails to meet expectations;

have significant customer impacts;

or

have a significant impact on a banking

organization’s financial condition or operations.

It is up to each banking organization to identify its

critical activities and third-party relationships that support these

critical activities. Notably, an activity that is critical for one

banking organization may not be critical for another. Some banking

organizations may assign a criticality or risk level to each third-party

relationship, whereas others identify critical activities and those

third parties that support such activities. Regardless of a banking

organization’s approach, a key element of effective risk management

is applying a sound methodology to designate which activities and

third-party relationships receive more comprehensive oversight.

C. Third-Party Relationship

Life Cycle

Effective third-party risk management

generally follows a continuous life cycle for third-party relationships.

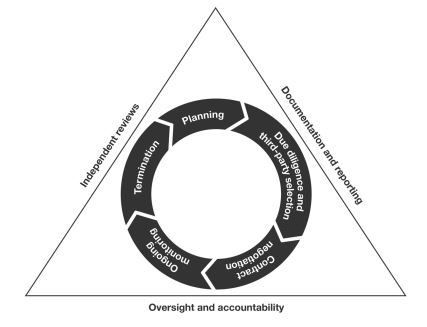

The stages of the risk management life cycle of third-party relationships

are shown in figure 1 and detailed below. The degree to which the

examples of considerations discussed in this guidance are relevant

to each banking organization is based on specific facts and circumstances

and these examples may not apply to all of a banking organization’s

third-party relationships.

It is important to involve staff with the requisite knowledge

and skills in each stage of the risk management life cycle. A banking

organization may involve experts across disciplines, such as compliance,

risk, or technology, as well as legal counsel, and may engage external

support when helpful to supplement the qualifications and technical

expertise of in-house staff.7

Figure 1. Stages of the Risk Management Life Cycle

Source: Board, FDIC, and OCC.

1. Planning

As part of sound risk management, effective planning allows a banking

organization to evaluate and consider how to manage risks before entering

into a third-party relationship. Certain third parties, such as those

that support a banking organization’s higher-risk activities, including

critical activities, typically warrant a greater degree of planning

and consideration. For example, when critical activities are involved,

plans may be presented to and approved by a banking organization’s

board of directors (or a designated board committee).

Depending on the degree of risk and complexity

of the third-party relationship, a banking organization typically

considers the following factors, among others, in planning:

understanding the strategic purpose

of the business arrangement and how the arrangement aligns with a

banking organization’s overall strategic goals, objectives, risk appetite,

risk profile, and broader corporate policies;

identifying and assessing the benefits

and the risks associated with the business arrangement and determining

how to appropriately manage the identified risks;

considering the nature of the business

arrangement, such as volume of activity, use of subcontractor(s),

technology needed, interaction with customers, and use of foreign-based

third parties;8

evaluating the estimated costs, including

estimated direct contractual costs and indirect costs expended to

augment or alter banking organization staffing, systems, processes,

and technology;

evaluating how the third-party relationship

could affect banking organization employees, including dual employees,9 and what transition steps are needed

for the banking organization to manage the impacts when activities

currently conducted internally are outsourced;

assessing a potential third party’s

impact on customers, including access to or use of those customers’

information, third-party interaction with customers, potential for

consumer harm, and handling of customer complaints and inquiries;

understanding potential information

security implications, including access to the banking organization’s

systems and to its confidential information;

understanding potential physical security

implications, including access to the banking organization’s facilities;

determining how the banking organization

will select, assess, and oversee the third party, including monitoring

the third party’s compliance with applicable laws, regulations, and

contractual provisions, and requiring remediation of compliance issues

that may arise;

determining the banking organization’s

ability to provide adequate oversight and management of the proposed

third-party relationship on an ongoing basis (including whether staffing

levels and expertise, risk management and compliance management systems,

organizational structure, policies and procedures, or internal control

systems need to be adapted over time for the banking organization

to effectively address the business arrangement); and

outlining the banking organization’s

contingency plans in the event the banking organization needs to transition

the activity to another third party or bring it in-house.

2. Due Diligence

and Third-Party Selection

Conducting

due diligence on third parties before selecting and entering into

third-party relationships is an important part of sound risk management.

It provides management with the information needed about potential

third parties to determine if a relationship would help achieve a

banking organization’s strategic and financial goals. The due diligence

process also provides the banking organization with the information

needed to evaluate whether it can appropriately identify, monitor,

and control risks associated with the particular third-party relationship.

Due diligence includes assessing the third party’s ability to: perform

the activity as expected, adhere to a banking organization’s policies

related to the activity, comply with all applicable laws and regulations,

and conduct the activity in a safe and sound manner. Relying solely

on experience with or prior knowledge of a third party is not an adequate

proxy for performing appropriate due diligence, as due diligence should

be tailored to the specific activity to be performed by the third

party.

The scope and degree of due diligence should be commensurate

with the level of risk and complexity of the third-party relationship.

More comprehensive due diligence is particularly important when a

third party supports higher-risk activities, including critical activities.

If a banking organization uncovers information that warrants additional

scrutiny, the banking organization should consider broadening the

scope or assessment methods of the due diligence.

In some instances, a banking organization may

not be able to obtain the desired due diligence information from a

third party. For example, the third party may not have a long operational

history, may not allow onsite visits, or may not share (or be permitted

to share) information that a banking organization requests. While

the methods and scope of due diligence may differ, it is important

for the banking organization to identify and document any limitations

of its due diligence, understand the risks from such limitations,

and consider alternatives as to how to mitigate the risks. In such

situations, a banking organization may, for example, obtain alternative

information to assess the third party, implement additional controls

on or monitoring of the third party to address the information limitation,

or consider using a different third party.

A banking organization may use the services of industry

utilities or consortiums, consult with other organizations,10 or engage in joint efforts to supplement its due diligence.

As the activity to be performed by the third party may present a different

level of risk to each banking organization, it is important to evaluate

the conclusions from such supplemental efforts based on the banking

organization’s own specific circumstances and performance criteria

for the activity. Effective risk-management processes include evaluating

the capabilities of any external party conducting the supplemental

efforts, understanding how such supplemental efforts relate to the

banking organization’s planned use of the third party, and assessing

the risks of relying on the supplemental efforts. Use of such external

parties to conduct supplemental due diligence does not abrogate the

responsibility of the banking organization to manage third-party relationships

in a safe and sound manner and consistent with applicable laws and

regulations.

Depending on the degree of risk and complexity of the

third-party relationship, a banking organization typically considers

the following factors, among others, as part of due diligence:

a. Strategies and goals. A review of the third

party’s overall business strategy and goals helps the banking organization

to understand: (1) how the third party’s current and proposed strategic

business arrangements (such as mergers, acquisitions, and partnerships)

may affect the activity; and (2) the third party’s service philosophies,

quality initiatives, and employment policies and practices (including

its diversity policies and practices). Such information may assist

a banking organization to determine whether the third party can perform

the activity in a manner that is consistent with the banking organization’s

broader corporate policies and practices.

b. Legal and regulatory compliance. A review of

any legal and regulatory compliance considerations associated with

engaging a third party allows a banking organization to evaluate whether

it can appropriately mitigate risks associated with the third-party

relationship. This may include (1) evaluating the third party’s ownership

structure (including identifying any beneficial ownership, whether

public or private, foreign, or domestic ownership) and whether the

third party has the necessary legal authority to perform the activity,

such as any necessary licenses or corporate powers; (2) determining

whether the third party itself or any owners are subject to sanctions

by the Office of Foreign Assets Control; (3) determining whether the

third party has the expertise, processes, and controls to enable the

banking organization to remain in compliance with applicable domestic

and international laws and regulations; (4) considering the third

party’s responsiveness to any compliance issues (including violations

of law or regulatory actions) with applicable supervisory agencies

and self-regulatory organizations, as appropriate; and (5) considering

whether the third party has identified, and articulated a process

to mitigate, areas of potential consumer harm.

c. Financial condition. An assessment

of a third party’s financial condition through review of available

financial information, including audited financial statements, annual

reports, and filings with the U.S. Securities and Exchange Commission

(SEC), among others, helps a banking organization evaluate whether

the third party has the financial capability and stability to perform

the activity. Where relevant and available, a banking organization

may consider other types of information such as access to funds, expected

growth, earnings, pending litigation, unfunded liabilities, reports

from debt rating agencies, and other factors that may affect the third

party’s overall financial condition.

d. Business experience. An evaluation of a third

party’s: (1) depth of resources (including staffing); (2) previous

experience in performing the activity; and (3) history of addressing

customer complaints or litigation and subsequent outcomes, helps to

inform a banking organization’s assessment of the third party’s ability

to perform the activity effectively. Another consideration may include

whether there have been significant changes in the activities offered

or in its business model. Likewise, a review of the third party’s

websites, marketing materials, and other information related to banking

products or services may help determine if statements and assertions

accurately represent the activities and capabilities of the third

party.

e. Qualifications and backgrounds of key personnel

and other human resources considerations. An evaluation of the

qualifications and experience of a third party’s principals and other

key personnel related to the activity to be performed provides insight

into the capabilities of the third party to successfully perform the

activities. An important consideration is whether the third party

and the banking organization, as appropriate, periodically conduct

background checks on the third party’s key personnel and contractors

who may have access to information technology systems or confidential

information. Another important consideration is whether there are

procedures in place for identifying and removing the third party’s

employees who do not meet minimum suitability requirements or are

otherwise barred from working in the financial services sector. Another

consideration is whether the third party has training to ensure that

its employees understand their duties and responsibilities and are

knowledgeable about applicable laws and regulations as well as other

factors that could affect performance or pose risk to the banking

organization. Finally, an evaluation of the third party’s succession

and redundancy planning for key personnel, and of the third party’s

processes for holding employees accountable for compliance with policies

and procedures, provides valuable information to the banking organization.

f. Risk management. Appropriate due diligence includes

an evaluation of the effectiveness of a third party’s overall risk

management, including policies, processes, and internal controls,

and alignment with applicable policies and expectations of the banking

organization surrounding the activity. This would include an assessment

of the third party’s governance processes, such as the establishment

of clear roles, responsibilities, and segregation of duties pertaining

to the activity. It is also important to consider whether the third

party’s controls and operations are subject to effective audit assessments,

including independent testing and objective reporting of results and

findings. Banking organizations also gain important insight by evaluating

processes for escalating, remediating, and holding management accountable

for concerns identified during audits, internal compliance reviews,

or other independent tests, if available. When relevant and available,

a banking organization may consider reviewing System and Organization

Control (SOC) reports and any conformity assessment or certification

by independent third parties related to relevant domestic or international

standards.11 In such cases, the banking organization

may also consider whether the scope and the results of the SOC reports,

certifications, or assessments are relevant to the activity to be

performed or suggest that additional scrutiny of the third party or

any of its contractors may be appropriate.

g. Information security. Understanding potential

information security implications, including access to a banking organization’s

systems and information, can help a banking organization decide whether

or not to engage with a third party. Due diligence in this area typically

involves assessing the third party’s information security program,

including its consistency with the banking organization’s information

security program, such as its approach to protecting the confidentiality,

integrity, and availability of the banking organization’s data. It

may also involve determining whether there are any gaps that present

risk to the banking organization or its customers and considering

the extent to which the third party applies controls to limit access

to the banking organization’s data and transactions, such as multifactor

authentication, end-to-end encryption, and secure source code management.

It also aids a banking organization when determining whether the third

party keeps informed of, and has sufficient experience in identifying,

assessing, and mitigating, known and emerging threats and vulnerabilities.

As applicable, assessing the third party’s data, infrastructure, and

application security programs, including the software development

life cycle and results of vulnerability and penetration tests, can

provide valuable information regarding information technology system

vulnerabilities. Finally, due diligence can help a banking organization

evaluate the third party’s implementation of effective and sustainable

corrective actions to address any deficiencies discovered during testing.

h. Management of information systems. It is important

to review and understand the third party’s business processes and

information systems that will be used to support the activity. When

technology is a major component of the third-party relationship, an

effective practice is to review both the banking organization’s and

the third party’s information systems to identify gaps in service-level

expectations, business process and management, and interoperability

issues. It is also important to review the third party’s processes

for maintaining timely and accurate inventories of its technology

and its contractor(s). A banking organization also benefits from understanding

the third party’s measures for assessing the performance of its information

systems.

i. Operational resilience. An assessment of a third

party’s operational resilience practices supports a banking organization’s

evaluation of a third party’s ability to effectively operate through

and recover from any disruption or incidents, both internal and external.12 Such an assessment is particularly important where the impact

of such disruption could have an adverse effect on the banking organization

or its customers, including when the third party interacts with customers.

It is important to assess options to employ if the third party’s ability

to perform the activity is impaired and to determine whether the third

party maintains appropriate operational resilience and cybersecurity

practices, including disaster recovery and business continuity plans

that specify the time frame to resume activities and recover data.

To gain additional insight into a third party’s resilience capabilities,

a banking organization may review (1) the results of operational resilience

and business continuity testing and performance during actual disruptions;

(2) the third party’s telecommunications redundancy and resilience

plans; and (3) preparations for known and emerging threats and vulnerabilities,

such as wide-scale natural disasters, pandemics, distributed denial

of service attacks, or other intentional or unintentional events.

Other considerations related to operational resilience include (1)

dependency on a single provider for multiple activities; and (2) interoperability

or potential end of life issues with the software programming language,

computer platform, or data storage technologies used by the third

party.

j. Incident reporting and management processes.

Review and consideration of a third party’s incident reporting and

management processes is helpful to determine whether there are clearly

documented processes, timelines, and accountability for identifying,

reporting, investigating, and escalating incidents. Such review assists

in confirming that the third party’s escalation and notification processes

meet the banking organization’s expectations and regulatory requirements.13

k. Physical security. It is important to evaluate

whether the third party has sufficient physical and environmental

controls to protect the safety and security of people (such as employees

and customers), its facilities, technology systems, and data, as applicable.

This would typically include a review of the third party’s employee

on- and off-boarding procedures to ensure that physical access rights

are managed appropriately.

l. Reliance on subcontractors.14 An evaluation of the volume

and types of subcontracted activities and the degree to which the

third party relies on subcontractors helps inform whether such subcontracting

arrangements pose additional or heightened risk to a banking organization.

This typically includes an assessment of the third party’s ability

to identify, manage, and mitigate risks associated with subcontracting,

including how the third party selects and oversees its subcontractors

and ensures that its subcontractors implement effective controls.

Other important considerations include whether additional risk is

presented by the geographic location of a subcontractor or dependency

on a single provider for multiple activities.

m. Insurance coverage. An evaluation of whether

the third party has existing insurance coverage helps a banking organization

determine the extent to which potential losses are mitigated, including

losses posed by the third party to the banking organization or that

might prevent the third party from fulfilling its obligations to the

banking organization. Such losses may be attributable to dishonest

or negligent acts; fire, floods, or other natural disasters; loss

of data; and other matters. Examples of insurance coverage may include

fidelity bond; liability; property hazard and casualty; and areas

that may not be covered under a general commercial policy, such as

cybersecurity or intellectual property.

n. Contractual arrangements with other parties.

A third party’s commitments to other parties may introduce potential

legal, financial, or operational implications to the banking organization.

Therefore, it is important to obtain and evaluate information regarding

the third party’s legally binding arrangements with subcontractors

or other parties to determine whether such arrangements may create

or transfer risks to the banking organization or its customers.

3. Contract Negotiation

When evaluating whether to enter into

a relationship with a third party, a banking organization typically

determines whether a written contract is needed, and if the proposed

contract can meet the banking organization’s business goals and risk-management

needs. After such determination, a banking organization typically

negotiates contract provisions that will facilitate effective risk

management and oversight and that specify the expectations and obligations

of both the banking organization and the third party. A banking organization

may tailor the level of detail and comprehensiveness of such contract

provisions based on the risk and complexity posed by the particular

third-party relationship.

While third parties may initially offer a standard contract,

a banking organization may seek to request modifications, additional

contract provisions, or addendums to satisfy its needs. In difficult

contract negotiations, including when a banking organization has limited

negotiating power, it is important for the banking organization to

understand any resulting limitations and consequent risks. Possible

actions that a banking organization might take in such circumstances

include determining whether the contract can still meet the banking

organization’s needs, whether the contract would result in increased

risk to the banking organization, and whether residual risks are acceptable.

If the contract is unacceptable for the banking organization, it may

consider other approaches, such as employing other third parties or

conducting the activity in-house. In certain circumstances, banking

organizations may gain an advantage by negotiating contracts as a

group with other organizations.

It is important that a banking organization understand

the benefits and risks associated with engaging third parties and

particularly before executing contracts involving higher-risk activities,

including critical activities. As part of its oversight responsibilities,

the board of directors should be aware of and, as appropriate, may

approve or delegate approval of contracts involving higher-risk activities.

Legal counsel review may also be warranted prior to finalization.

Periodic reviews of executed contracts allow a banking

organization to confirm that existing provisions continue to address

pertinent risk controls and legal protections. If new risks are identified,

a banking organization may consider renegotiating a contract.

Depending on the degree of risk

and complexity of the third-party relationship, a banking organization

typically considers the following factors, among others, during contract

negotiations:

a. Nature and scope of arrangement. In negotiating

a contract, it is helpful for a banking organization to clearly identify

the rights and responsibilities of each party. This typically includes

specifying the nature and scope of the business arrangement. Additional

considerations may also include, as applicable, a description of (1)

ancillary services such as software or other technology support, maintenance,

and customer service; (2) the activities the third party will perform;

and (3) the terms governing the use of the banking organization’s

information, facilities, personnel, systems, intellectual property,

and equipment, as well as access to and use of the banking organization’s

or customers’ information. If dual employees will be used, it may

also be helpful to specify their responsibilities and reporting lines.

It is also important for a banking organization to understand how

changes in business and other circumstances may give rise to the third

party’s rights to terminate or renegotiate the contract.

b. Performance measures or benchmarks. For certain relationships, clearly defined performance measures

can assist a banking organization in evaluating the performance of

a third party. In particular, a service-level agreement between the

banking organization and the third party can help specify the measures

surrounding the expectations and responsibilities for both parties,

including conformance with policies and procedures and compliance

with applicable laws and regulations. Such measures can be used to

monitor performance, penalize poor performance, or reward outstanding

performance. It is important to negotiate performance measures that

do not incentivize imprudent performance or behavior, such as encouraging

processing volume or speed without regard for accuracy, compliance

requirements, or adverse effects on the banking organization or customers.

c. Responsibilities for providing, receiving, and retaining

information. It is important to consider contract provisions that

specify the third party’s obligation for retention and provision of

timely, accurate, and comprehensive information to allow the banking

organization to monitor risks and performance and to comply with applicable

laws and regulations. Such provisions typically address:

the banking organization’s ability

to access its data in an appropriate and timely manner;

the banking organization’s access

to, or use of, the third party’s data and any supporting documentation,

in connection with the business arrangement;

the banking organization’s access to,

or use of, its own or the third party’s data and how such data and

supporting documentation may be shared with regulators in a timely

manner as part of the supervisory process;

whether the third party is permitted

to resell, assign, or permit access to customer data, or the banking

organization’s data, metadata, and systems, to other entities;

notification to the banking organization

whenever compliance lapses, enforcement actions, regulatory proceedings,

or other events pose a significant risk to the banking organization

or customers;

notification to the banking organization

of significant strategic or operational changes, such as mergers,

acquisitions, divestitures, use of subcontractors, key personnel changes,

or other business initiatives that could affect the activities involved;

and

specification of the type and frequency

of reports to be received from the third party, as appropriate. This

may include performance reports, financial reports, security reports,

and control assessments.

d. The right to audit and require remediation.

To help ensure that a banking organization has the ability to monitor

the performance of a third party, a contract often establishes the

banking organization’s right to audit and provides for remediation

when issues are identified. Generally, a contract includes provisions

for periodic, independent audits of the third party and its relevant

subcontractors, consistent with the risk and complexity of the third-party

relationship. Therefore, it would be appropriate to consider whether

contract provisions describe the types and frequency of audit reports

the banking organization is entitled to receive from the third party

(for example, SOC reports, Payment Card Industry (PCI) compliance

reports, or other financial and operational reviews). Such contract

provisions may also reserve the banking organization’s right to conduct

its own audits of the third party’s activities or to engage an independent

party to perform such audits.

e. Responsibility for compliance with applicable laws

and regulations. A banking organization is responsible for conducting

its activities in compliance with applicable laws and regulations,

including those activities involving third parties. The use of third

parties does not abrogate these responsibilities. Therefore, it is

important for a contract to specify the obligations of the third party

and the banking organization to comply with applicable laws and regulations.

It is also important for the contract to provide the banking organization

with the right to monitor and be informed about the third party’s

compliance with applicable laws and regulations, and to require timely

remediation if issues arise. Contracts may also reflect considerations

of relevant guidance and self-regulatory standards, where applicable.

f. Costs and compensation. Contracts that clearly

describe all costs and compensation arrangements help reduce misunderstandings

and disputes over billing and help ensure that all compensation arrangements

are consistent with sound banking practices and applicable laws and

regulations. Contracts commonly describe compensation and fees, including

cost schedules, calculations for base services, and any fees based

on volume of activity and for special requests. Contracts also may

specify the conditions under which the cost structure may be changed,

including limits on any cost increases. During negotiations, a banking

organization should confirm that a contract does not include incentives

that promote inappropriate risk taking by the banking organization

or the third party. A banking organization should also consider whether

the contract includes burdensome upfront or termination fees, or provisions

that may require the banking organization to reimburse the third party.

Appropriate provisions indicate which party is responsible for payment

of legal, audit, and examination fees associated with the activities

involved. Another consideration is outlining cost and responsibility

for purchasing and maintaining hardware and software, where applicable.

g. Ownership and license. In order to prevent disputes

between the parties regarding the ownership and licensing of a banking

organization’s property, it is common for a contract to state the

extent to which the third party has the right to use the banking organization’s

information, technology, and intellectual property, such as the banking

organization’s name, logo, trademark, and copyrighted material. Provisions

that indicate whether any data generated by the third party become

the banking organization’s property help avert misunderstandings.

It is also important to include appropriate warranties on the part

of the third party related to its acquisition of licenses or subscriptions

for use of any intellectual property developed by other third parties.

When the banking organization purchases software, it is important

to consider a provision to establish escrow agreements to provide

for the banking organization’s access to source code and programs

under certain conditions (for example, insolvency of the third party).

h. Confidentiality and integrity. With respect

to contracts with third parties, there may be increased risks related

to the sensitivity of non-public information or access to infrastructure.

Effective contracts typically prohibit the use and disclosure of banking

organization and customer information by a third party and its subcontractors,

except as necessary to provide the contracted activities or comply

with legal requirements. If the third party receives personally identifiable

information, contract provisions are important to ensure that the

third party implements and maintains appropriate security measures

to comply with applicable laws and regulations.

Another important provision is one that specifies

when and how the third party will disclose, in a timely manner, information

security breaches or unauthorized intrusions. Considerations may include

the types of data stored by the third party, legal obligations for

the banking organization to disclose the breach to its regulators

or customers, the potential for consumer harm, or other factors. Such

provisions typically stipulate that the data intrusion notification

to the banking organization include estimates of the effects on the

banking organization and its customers and specify corrective action

to be taken by the third party. They also address the powers of each

party to change security and risk-management procedures and requirements

and resolve any confidentiality and integrity issues arising out of

shared use of facilities owned by the third party. Typically, such

provisions stipulate whether and how often the banking organization

and the third party will jointly practice incident management exercises

involving unauthorized intrusions or other breaches of confidentiality

and integrity.

i. Operational resilience and business continuity. Both internal and external factors or incidents (for example, natural

disasters or cyber incidents) may affect a banking organization or

a third party and thereby disrupt the third party’s performance of

the activity. Consequently, an effective contract provides for continuation

of the activity in the event of problems affecting the third party’s

operations, including degradations or interruptions in delivery. As

such, it is important for the contract to address the third party’s

responsibility for appropriate controls to support operational resilience

of the services, such as protecting and storing programs, backing

up datasets, addressing cybersecurity issues, and maintaining current

and sound business resumption and business continuity plans.

To help ensure maintenance of operations,

contracts often require the third party to provide the banking organization

with operating procedures to be carried out in the event business

continuity plans are implemented, including specific recovery time

and recovery point objectives. Contracts may also stipulate whether

and how often the banking organization and the third party will jointly

test business continuity plans. Another consideration is whether the

contract provides for the transfer of the banking organization’s accounts,

data, or activities to another third party without penalty in the

event of the third party’s bankruptcy, business failure, or business

interruption.

j. Indemnification and limits on liability. Incorporating

indemnification provisions into a contract may reduce the potential

for a banking organization to be held liable for claims and be reimbursed

for damages arising from a third party’s misconduct, including negligence

and violations of laws and regulations. As such, it is important to

consider whether indemnification clauses specify the extent to which

the banking organization will be held liable for claims or be reimbursed

for damages based on the failure of the third party or its subcontractor

to perform, including failure of the third party to obtain any necessary

intellectual property licenses. Such consideration typically includes

an assessment of whether any limits on liability are in proportion

to the amount of loss the banking organization might experience as

a result of third-party failures, or whether indemnification clauses

require the banking organization to hold the third party harmless

from liability.

k. Insurance. One way in which a banking organization

can protect itself against losses caused by or related to a third

party and the products and services provided through third-party relationships

is by including insurance requirements in a contract. These provisions

typically require the third party to (1) maintain specified types

and amounts of insurance (including, if appropriate, naming the banking

organization as insured or additional insured); (2) notify the banking

organization of material changes to coverage; and (3) provide evidence

of coverage, as appropriate. The type and amount of insurance coverage

should be commensurate with the risk of possible losses, including

those caused by the third party to the banking organization or that

might prevent the third party from fulfilling its obligations to the

banking organization, and the activities performed.

l. Dispute resolution. Disputes

regarding a contract can delay or otherwise have an adverse impact

upon the activities performed by a third party, which may negatively

affect the banking organization. Therefore, a banking organization

may want to consider whether the contract should establish a dispute

resolution process to resolve problems between the banking organization

and the third party in an expeditious manner, and whether the third

party should continue to provide activities to the banking organization

during the dispute resolution period. It is important to also understand

whether the contract contains provisions that may impact the banking

organization’s ability to resolve disputes in a satisfactory manner,

such as provisions addressing arbitration or forum selection.

m. Customer complaints. Where

customer interaction is an important aspect of the third-party relationship,

a banking organization may find it useful to include a contract provision

to ensure that customer complaints and inquiries are handled properly.

Effective contracts typically specify whether the banking organization

or the third party is responsible for responding to customer complaints

or inquiries. If it is the third party’s responsibility, it is important

to include provisions for the third party to receive and respond to

customer complaints and inquiries in a timely manner and to provide

the banking organization with sufficient, timely, and usable information

to analyze customer complaint and inquiry activity and associated

trends. If it is the banking organization’s responsibility, it is

important to include provisions for the banking organization to receive

prompt notification from the third party of any complaints or inquiries

received by the third party.

n. Subcontracting. Third-party relationships may

involve subcontracting arrangements, which can result in risk due

to the absence of a direct relationship between the banking organization

and the subcontractor, further lessening the banking organization’s

direct control of activities. The impact on a banking organization’s

ability to assess and control risks may be especially important if

the banking organization uses third parties for higher-risk activities,

including critical activities. For this reason, a banking organization

may want to address when and how the third party should notify the

banking organization of its use or intent to use a subcontractor and

whether specific subcontractors are prohibited by the banking organization.

Another important consideration is whether the contract should prohibit

assignment, transfer, or subcontracting of the third party’s obligations

to another entity without the banking organization’s consent. Where

subcontracting is integral to the activity being performed for the

banking organization, it is important to consider more detailed contractual

obligations, such as reporting on the subcontractor’s conformance

with performance measures, periodic audit results, and compliance

with laws and regulations. Where appropriate, a banking organization

may consider including a provision that states the third party’s liability

for activities or actions by its subcontractors and which party is

responsible for the costs and resources required for any additional

monitoring and management of the subcontractors. It may also be appropriate

to reserve the right to terminate the contract without penalty if

the third party’s subcontracting arrangements do not comply with contractual

obligations.

o. Foreign-based third parties. In contracts with

foreign-based third parties, it is important to consider choice-of-law

and jurisdictional provisions that provide dispute adjudication under

the laws of a single jurisdiction, whether in the United States or

elsewhere. When engaging with foreign-based third parties, or where

contracts include a choice-of-law provision that includes a jurisdiction

other than the United States, it is important to understand that such

contracts and covenants may be subject to the interpretation of foreign

courts relying on laws in those jurisdictions. It may be warranted

to seek legal advice on the enforceability of the proposed contract

with a foreign-based third party and other legal ramifications, including

privacy laws and cross-border flow of information.

p. Default and termination. Contracts

can protect the ability of the banking organization to change third

parties when appropriate without undue restrictions, limitations,

or cost. An effective contract stipulates what constitutes default,

identifies remedies, allows opportunities to cure defaults, and establishes

the circumstances and responsibilities for termination.

Therefore, it is important to consider including contractual

provisions that:

provide termination and notification

requirements with reasonable time frames to allow for the orderly

transition of the activity, when desired or necessary, without prohibitive

expense;

provide for the timely return or destruction

of the banking organization’s data, information, and other resources;

assign all costs and obligations associated

with transition and termination; and

enable the banking organization to

terminate the relationship with reasonable notice and without penalty,

if formally directed by the banking organization’s primary federal

banking regulator.

q. Regulatory supervision. For relevant third-party

relationships, it is important for contracts to stipulate that the

performance of activities by third parties for the banking organization

is subject to regulatory examination and oversight, including appropriate

retention of, and access to, all relevant documentation and other

materials.15 This can help ensure that a third party is aware of its role

and potential liability in its relationship with a banking organization.

4. Ongoing Monitoring

Ongoing monitoring enables a banking organization

to: (1) confirm the quality and sustainability of a third party’s

controls and ability to meet contractual obligations; (2) escalate

significant issues or concerns, such as material or repeat audit findings,

deterioration in financial condition, security breaches, data loss,

service interruptions, compliance lapses, or other indicators of increased

risk; and (3) respond to such significant issues or concerns when

identified.

Effective third-party risk management includes ongoing

monitoring throughout the duration of a third-party relationship,

commensurate with the level of risk and complexity of the relationship

and the activity performed by the third party. Ongoing monitoring

may be conducted on a periodic or continuous basis, and more comprehensive

or frequent monitoring is appropriate when a third-party relationship

supports higher-risk activities, including critical activities. Because

both the level and types of risks may change over the lifetime of

third-party relationships, banking organizations may adapt their ongoing

monitoring practices accordingly, including changes to the frequency

or type of information used in monitoring.

Typical monitoring activities include: (1) review of reports

regarding the third party’s performance and the effectiveness of its

controls; (2) periodic visits and meetings with third-party representatives

to discuss performance and operational issues; and (3) regular testing

of the banking organization’s controls that manage risks from its

third-party relationships, particularly when supporting higher-risk

activities, including critical activities. In certain circumstances,

based on risk, a banking organization may also perform direct testing

of the third party’s own controls. To gain efficiencies or leverage

specialized expertise, banking organizations may engage external resources,

refer to conformity assessments or certifications, or collaborate

when performing ongoing monitoring.16 To support effective monitoring,

a banking organization dedicates sufficient staffing with the necessary

expertise, authority, and accountability to perform a range of ongoing

monitoring activities, such as those described above.

Depending on the degree of risk and complexity

of the third-party relationship, a banking organization typically

considers the following factors, among others, as part of ongoing

monitoring:

the overall effectiveness of the

third-party relationship, including its consistency with the banking

organization’s strategic goals, business objectives, risk appetite,

risk profile, and broader corporate policies;

changes to the third party’s business

strategy and its agreements with other entities that may pose new

or increased risks or impact the third party’s ability to meet contractual

obligations;

changes in the third party’s financial

condition, including its financial obligations to others;

changes to, or lapses in, the third

party’s insurance coverage;

relevant audits, testing results,

and other reports that address whether the third party remains capable

of managing risks and meeting contractual obligations and regulatory

requirements;

the third party’s ongoing compliance

with applicable laws and regulations and its performance as measured

against contractual obligations;

changes in the third party’s key

personnel involved in the activity;

the third party’s reliance on, exposure

to, and use of subcontractors, the location of subcontractors (and

any related data), and the third party’s own risk management processes

for monitoring subcontractors;

training provided to employees of

the banking organization and the third party;

the third party’s response to changing

threats, new vulnerabilities, and incidents impacting the activity,

including any resulting adjustments to the third party’s operations

or controls;

the third party’s ability to maintain

the confidentiality, availability, and integrity of the banking organization’s

systems, information, and data, as well as customer data, where applicable;

the third party’s response to incidents,

business continuity and resumption plans, and testing results to evaluate

the third party’s ability to respond to and recover from service disruptions

or degradations;

factors and conditions external to

the third party that could affect its performance and financial and

operational standing, such as changing laws, regulations, and economic

conditions; and

the volume, nature, and trends of customer

inquiries and complaints, the adequacy of the third party’s responses

(if responsible for handling customer inquiries or complaints), and

any resulting remediation.

5. Termination

A banking organization may terminate a

relationship for various reasons, such as expiration or breach of

the contract, the third party’s failure to comply with applicable

laws or regulations, or a desire to seek an alternate third party,

bring the activity in-house, or discontinue the activity. When this

occurs, it is important for management to terminate relationships

in an efficient manner, whether the activities are transitioned to

another third party, brought in-house, or discontinued. Depending

on the degree of risk and complexity of the third-party relationship,

a banking organization typically considers the following factors,

among others, to facilitate termination:

options for an effective transition

of services, such as potential alternate third parties to perform

the activity;

relevant capabilities, resources,

and the time frame required to transition the activity to another

third party or bring in-house while still managing legal, regulatory,

customer, and other impacts that might arise;

costs and fees associated with termination;

managing risks associated with data

retention and destruction, information system connections and access

control, or other control concerns that require additional risk management

and monitoring after the end of the third-party relationship;

handling of joint intellectual property;

and

managing risks to the banking organization,

including any impact on customers, if the termination happens as a

result of the third party’s inability to meet expectations.

D. Governance

There are a variety of ways for banking organizations

to structure their third-party risk-management processes. Some banking

organizations disperse accountability for their third-party risk-management

processes among their business lines.17 Other banking organizations may centralize the processes under

their compliance, information security, procurement, or risk management

functions. Regardless of how a banking organization structures its

process, the following practices are typically considered throughout

the third-party risk management life cycle,18 commensurate with risk and complexity.

1. Oversight and Accountability

Proper oversight and accountability are

important aspects of third-party risk management because they help

enable a banking organization to minimize adverse financial, operational,

or other consequences. A banking organization’s board of directors

has ultimate responsibility for providing oversight for third-party

risk management and holding management accountable. The board also

provides clear guidance regarding acceptable risk appetite, approves

appropriate policies, and ensures that appropriate procedures and

practices have been established. A banking organization’s management

is responsible for developing and implementing third-party risk management

policies, procedures, and practices, commensurate with the banking

organization’s risk appetite and the level of risk and complexity

of its third-party relationships.

In carrying out its responsibilities, the board of directors

(or a designated board committee) typically considers the following

factors, among others:

whether third-party relationships

are managed in a manner consistent with the banking organization’s

strategic goals and risk appetite and in compliance with applicable

laws and regulations;

whether there is appropriate periodic

reporting on the banking organization’s third-party relationships,

such as the results of management’s planning, due diligence, contract

negotiation, and ongoing monitoring activities; and

whether management has taken appropriate

actions to remedy significant deterioration in performance or address

changing risks or material issues identified, including through ongoing

monitoring and independent reviews.

When carrying out its responsibilities, management typically

performs the following activities, among others:

integrating third-party risk management

with the banking organization’s overall risk-management processes;

directing planning, due diligence,

and ongoing monitoring activities;

reporting periodically to the board

(or designated committee), as appropriate, on third-party risk-management

activities;

providing that contracts with third

parties are appropriately reviewed, approved, and executed;

establishing appropriate organizational

structures and staffing (level and expertise) to support the banking

organization’s third-party risk-management processes;

implementing and maintaining an appropriate

system of internal controls to manage risks associated with third-party

relationships;

assessing whether the banking organization’s

compliance management system is appropriate to the nature, size, complexity,

and scope of its third-party relationships;

determining whether the banking organization

has appropriate access to data and information from its third parties;

escalating significant issues to

the board and monitoring any resulting remediation, including actions

taken by the third party; and

terminating business arrangements

with third parties when they do not meet expectations or no longer

align with the banking organization’s strategic goals, objectives,

or risk appetite.

2. Independent

Reviews

It is important for a banking

organization to conduct periodic independent reviews to assess the

adequacy of its third-party risk-management processes. Such reviews

typically consider the following factors, among others:

whether the third-party relationships

align with the banking organization’s business strategy, and with

internal policies, procedures, and standards;

whether risks of third-party relationships

are identified, measured, monitored, and controlled;

whether the banking organization’s

processes and controls are designed and operating adequately;

whether appropriate staffing and expertise

are engaged to perform risk management activities throughout the third-party

risk management life cycle, including involving multiple disciplines

across the banking organization, as appropriate; and

whether conflicts of interest or appearances

of conflicts of interest are avoided or eliminated when selecting

or overseeing third parties.

A banking organization may use the results of independent

reviews to determine whether and how to adjust its third-party risk-management

process, including its policies, reporting, resources, expertise,

and controls. It is important that management respond promptly and

thoroughly to issues or concerns identified and escalate them to the

board, as appropriate.

3. Documentation and Reporting

It

is important that a banking organization properly document and report

on its third-party risk management process and specific third-party

relationships throughout their life cycle. Documentation and reporting,

key elements that assist those within or outside the banking organization

who conduct control activities, will vary among banking organizations

depending on the risk and complexity of their third-party relationships.

Examples of processes that support effective documentation and internal

reporting that the agencies have observed include, but are not limited

to:

a current inventory of all third-party

relationships (and, as appropriate to the risk presented, related

subcontractors) that clearly identifies those relationships associated

with higher-risk activities, including critical activities;

planning and risk assessments related

to the use of third parties;

due diligence results and recommendations;

executed contracts;

remediation plans and related reports

addressing the quality and sustainability of the third party’s controls;

risk and performance reports required

and received from the third party as part of ongoing monitoring;

if applicable, reports related to

customer complaint and inquiry monitoring, and any subsequent remediation

reports;

reports from third parties of service

disruptions, security breaches, or other events that pose, or may

pose, a material risk to the banking organization;

results of independent reviews; and

periodic reporting to the board (including,

as applicable, dependency on a single provider for multiple activities).

E. Supervisory Reviews

of Third-Party Relationships

The concepts

discussed in this guidance are relevant for all third-party relationships

and are provided to banking organizations to assist in the tailoring

and implementation of risk management practices commensurate to each

banking organization’s size, complexity, risk profile, and the nature

of its third-party relationships. Each agency will review its supervised

banking organizations’ risk management of third-party relationships

as part of its standard supervisory processes. Supervisory reviews

will evaluate risks and the effectiveness of risk management to determine

whether activities are conducted in a safe and sound manner and in

compliance with applicable laws and regulations.

In their evaluations of a banking organization’s

third-party risk management, examiners consider that banking organizations

engage in a diverse set of third-party relationships, that not all

third-party risk relationships present the same risks, and that banking

organizations accordingly tailor their practices to the risks presented.

Thus, the scope of the supervisory review depends on the degree of

risk and the complexity associated with the banking organization’s

activities and third-party relationships. When reviewing third-party

risk-management processes, examiners typically conduct the following

activities, among others:

assess the ability of the banking

organization’s management to oversee and manage the banking organization’s

third-party relationships;

assess the impact of third-party relationships

on the banking organization’s risk profile and key aspects of financial

and operational performance, including compliance with applicable

laws and regulations;

perform transaction testing or review

results of testing to evaluate the activities performed by the third

party and assess compliance with applicable laws and regulations;

highlight and discuss any material

risks and deficiencies in the banking organization’s risk management

process with senior management and the board of directors as appropriate;

review the banking organization’s

plans for appropriate and sustainable remediation of any deficiencies,

particularly those associated with the oversight of third parties

that involve critical activities; and

consider supervisory findings when

assigning the components of the applicable rating system and highlight

any material risks and deficiencies in the Report of Examination.

When circumstances warrant, an agency may use its legal

authority to examine functions or operations that a third party performs

on a banking organization’s behalf. Such examinations may evaluate

the third party’s ability to fulfill its obligations in a safe and

sound manner and comply with applicable laws and regulations, including

those designed to protect customers and to provide fair access to

financial services. The agencies may pursue corrective measures, including

enforcement actions, when necessary to address violations of laws

and regulations or unsafe or unsound banking practices by the banking

organization or its third party.

For a description of the banking organizations supervised

by each agency, refer to the definition of “appropriate federal banking

agency” in section 3(q) of the Federal Deposit Insurance Act (12 U.S.C.

1813(q)). This guidance is relevant to all banking organizations supervised

by the agencies.

Supervisory guidance does not have the force and

effect of law and does not impose any new requirements on banking

organizations. See 12 CFR 4, subpart F, appendix A (OCC); 12

CFR 262, appendix A (FRB); and 12 CFR 302, appendix A (FDIC).

See 12 U.S.C. 1831p–1. The agencies implemented

section 1831p–1 by regulation through the “Interagency Guidelines

Establishing Standards for Safety and Soundness.” See 12 CFR

part 30, appendix A (OCC); 12 CFR part 208, appendix D–1 (Board);

and 12 CFR part 364, appendix A (FDIC).

References to applicable laws and regulations throughout

this guidance include but are not limited to those designed to protect

consumers (such as fair lending laws and prohibitions against unfair,

deceptive or abusive acts or practices) and those addressing financial

crimes.

This guidance is relevant for all third-party relationships,

including situations in which a supervised banking organization provides

services to another supervised banking organization.

When a banking organization uses a third-party assessment

service or utility, it has a business arrangement with that entity.

Therefore, the arrangement should be incorporated into the banking

organization’s third-party risk-management processes.

The term “foreign-based third-party” refers to third

parties whose servicing operations are located in a foreign country

and subject to the law and jurisdiction of that country. Accordingly,

this term does not include a U.S.-based subsidiary of a foreign firm

because its servicing operations are subject to U.S. laws. This term

does include U.S. third parties to the extent that their actual servicing

operations are located in or subcontracted to entities domiciled in

a foreign country and subject to the law and jurisdiction of that

country.

For example, those of the National Institute of Standards

and Technology, Accredited Standards Committee X9, and the International

Standards Organization.

For example, regulatory requirements regarding incident

notification include the FBAs’ “Computer Security Incident Notification

Rule.” See 12 CFR part 53 (OCC); 12 CFR 225, subpart N (Board);

and 12 CFR 304, subpart C (FDIC).

Third parties may enlist the help of suppliers, service

providers, or other organizations, which this guidance collectively

refers to as subcontractors.

Refer to important considerations discussed in “Due

Diligence and Third-Party Selection” of this guidance when a banking

organization chooses to engage external resources to supplement its

third-party risk management.

Each applicable business line can provide valuable

input into the third-party risk management process, for example, by

completing risk assessments, reviewing due diligence information,

and evaluating the controls over the third-party relationship.